All Categories

Featured

Table of Contents

If you pick level term life insurance, you can allocate your costs because they'll remain the exact same throughout your term. Plus, you'll recognize precisely just how much of a survivor benefit your beneficiaries will receive if you pass away, as this amount will not alter either. The rates for degree term life insurance coverage will certainly depend upon several aspects, like your age, health condition, and the insurer you pick.

As soon as you go through the application and medical examination, the life insurance policy firm will certainly evaluate your application. They need to notify you of whether you have actually been approved soon after you apply. Upon authorization, you can pay your first costs and sign any pertinent documents to guarantee you're covered. From there, you'll pay your costs on a regular monthly or yearly basis.

Aflac's term life insurance policy is practical. You can select a 10, 20, or thirty years term and enjoy the added tranquility of mind you deserve. Dealing with an agent can help you find a plan that functions finest for your demands. Find out more and get a quote today!.

As you search for means to protect your economic future, you have actually likely come throughout a wide range of life insurance options. joint term life insurance. Selecting the appropriate coverage is a big decision. You wish to discover something that will certainly aid sustain your loved ones or the causes vital to you if something takes place to you

Lots of people favor term life insurance coverage for its simpleness and cost-effectiveness. Term insurance contracts are for a reasonably brief, defined period of time yet have options you can customize to your demands. Particular benefit alternatives can make your premiums transform over time. Level term insurance policy, nevertheless, is a kind of term life insurance policy that has constant repayments and a changeless.

Sought-After Annual Renewable Term Life Insurance

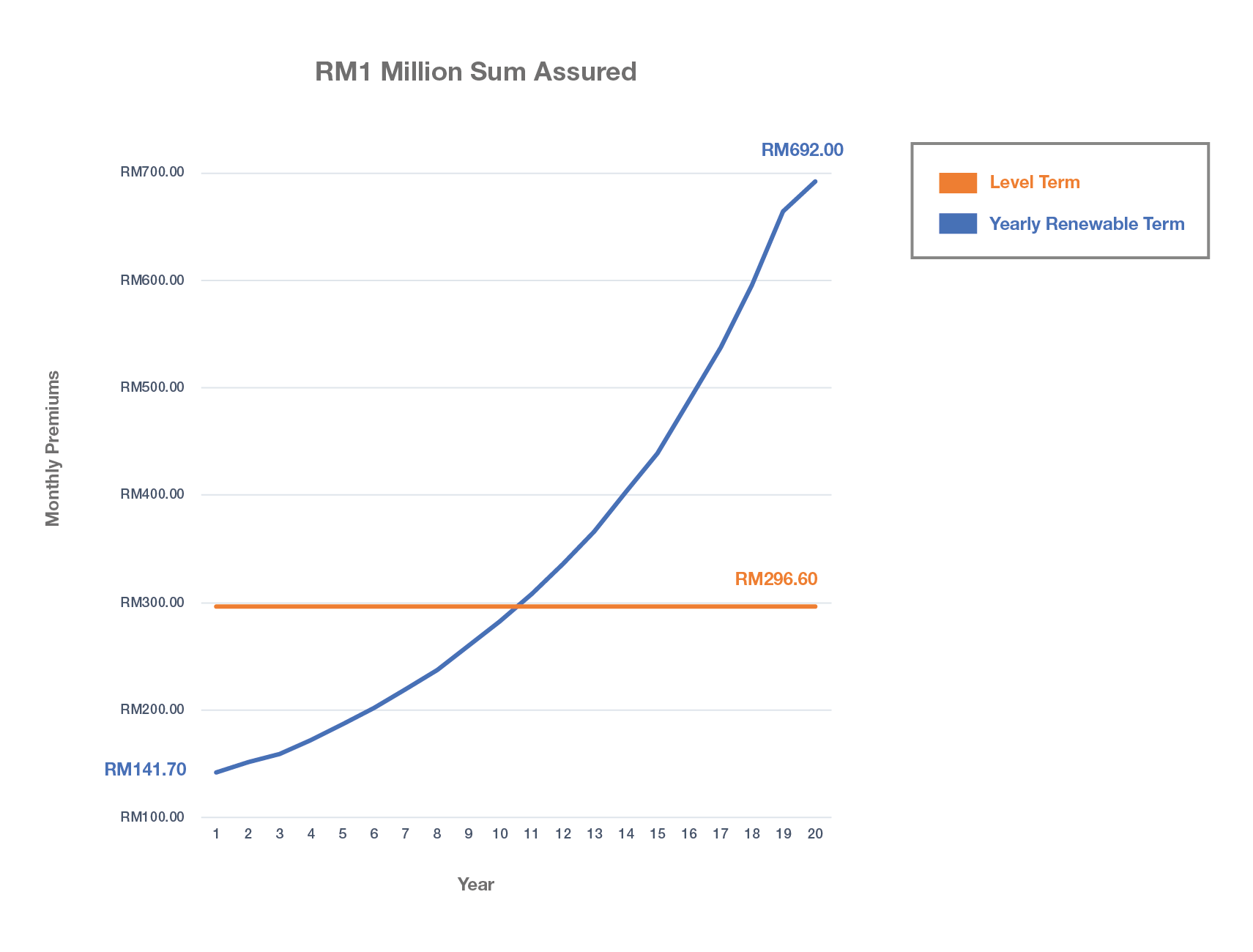

Degree term life insurance coverage is a subset of It's called "degree" because your costs and the benefit to be paid to your liked ones remain the very same throughout the contract. You will not see any type of adjustments in expense or be left questioning its value. Some agreements, such as annually renewable term, might be structured with premiums that increase with time as the insured ages.

Taken care of death benefit. This is additionally set at the start, so you can recognize specifically what death benefit amount your can anticipate when you pass away, as long as you're covered and up-to-date on costs.

This frequently between 10 and three decades. You consent to a set costs and fatality advantage throughout of the term. If you pass away while covered, your survivor benefit will be paid to loved ones (as long as your premiums depend on day). Your recipients will know beforehand exactly how much they'll get, which can help for preparing functions and bring them some economic protection.

You may have the choice to for another term or, more probable, renew it year to year. If your agreement has an ensured renewability provision, you may not require to have a new medical exam to maintain your protection going. However, your costs are most likely to increase due to the fact that they'll be based on your age at revival time (increasing term life insurance).

With this option, you can that will last the rest of your life. In this instance, once more, you might not need to have any brand-new medical exams, however costs likely will increase because of your age and brand-new coverage. annual renewable term life insurance. Various companies use various choices for conversion, be sure to recognize your selections prior to taking this step

Cost-Effective What Is Voluntary Term Life Insurance

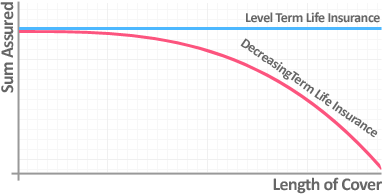

Talking with a monetary advisor additionally might aid you figure out the course that aligns best with your overall method. Most term life insurance policy is level term throughout of the contract period, yet not all. Some term insurance policy might feature a premium that boosts in time. With lowering term life insurance, your survivor benefit decreases over time (this kind is frequently secured to specifically cover a long-lasting debt you're paying off).

And if you're established for renewable term life, then your premium likely will go up yearly. If you're discovering term life insurance policy and intend to make sure simple and predictable financial security for your family members, level term may be something to take into consideration. Nonetheless, just like any kind of sort of insurance coverage, it might have some restrictions that do not meet your needs.

The Combination Of Whole Life And Term Insurance Is Referred To As A Family Income Policy

Generally, term life insurance policy is extra budget-friendly than irreversible coverage, so it's a cost-effective means to protect monetary defense. Adaptability. At the end of your agreement's term, you have numerous alternatives to continue or relocate on from protection, frequently without requiring a medical examination. If your budget plan or insurance coverage needs adjustment, death advantages can be lowered gradually and result in a lower premium.

As with various other kinds of term life insurance, when the agreement finishes, you'll likely pay greater premiums for protection because it will recalculate at your existing age and health. If your financial scenario modifications, you might not have the necessary insurance coverage and could have to buy extra insurance.

However that does not indicate it's a fit for everyone. As you're shopping for life insurance coverage, right here are a few crucial elements to consider: Budget plan. Among the advantages of level term insurance coverage is you know the price and the fatality benefit upfront, making it much easier to without stressing over increases in time.

Age and health and wellness. Generally, with life insurance policy, the healthier and younger you are, the more economical the insurance coverage. If you're young and healthy and balanced, it may be an appealing alternative to lock in low premiums now. Financial duty. Your dependents and financial duty play a role in identifying your protection. If you have a young household, as an example, degree term can assist provide financial backing throughout critical years without paying for coverage longer than needed.

1 All motorcyclists undergo the terms and conditions of the cyclist. All cyclists may not be readily available in all territories. Some states may differ the conditions (term life insurance with accidental death benefit). There may be an added fee connected with getting specific riders. Some riders may not be available in mix with other cyclists and/or policy functions.

2 A conversion debt is not available for TermOne plans. 3 See Term Conversions area of the Term Collection 160 Product Guide for how the term conversion credit history is determined. A conversion credit rating is not available if premiums or costs for the new plan will certainly be forgoed under the terms of a motorcyclist offering impairment waiver benefits.

Top Term Vs Universal Life Insurance

Plans transformed within the very first plan year will receive a prorated conversion debt topic to terms of the plan. 4 After 5 years, we reserve the right to restrict the irreversible product used. Term Series products are issued by Equitable Financial Life Insurance Firm (Equitable Financial) (NY, NY) and are co-distributed by Equitable Network, LLC (Equitable Network Insurance Policy Firm of The Golden State, LLC in CA; Equitable Network Insurance Policy Agency of Utah in UT; and Equitable Network of Puerto Rico, Inc. Term Life Insurance Policy is a sort of life insurance coverage policy that covers the insurance policy holder for a details amount of time, which is understood as the term. The term lengths differ according to what the individual selects. Terms generally range from 10 to 30 years and rise in 5-year increments, giving degree term insurance coverage.

{kind=link}

Latest Posts

Which Is The Best Funeral Plan

Final Expense Network Reviews

How To Pay For A Funeral With Life Insurance